Introduction to Standard Costing

Standard costing is an important subtopic of cost accounting. Standard costs are usually associated with a manufacturing company's costs of direct material, direct labor, and manufacturing overhead.Rather than assigning the actual costs of direct material, direct labor, and manufacturing overhead to a product, many manufacturers assign the expected or standard cost. This means that a manufacturer's inventories and cost of goods sold will begin with amounts reflecting the standard costs, not the actual costs, of a product. Manufacturers, of course, still have to pay the actual costs. As a result there are almost always differences between the actual costs and the standard costs, and those differences are known as variances.

Standard costing and the related variances is a valuable management tool. If a variance arises, management becomes aware that manufacturing costs have differed from the standard (planned, expected) costs.

- If actual costs are greater than standard costs the variance is unfavorable. An unfavorable variance tells management that if everything else stays constant the company's actual profit will be less than planned.

- If actual costs are less than standard costs the variance is favorable. A favorable variance tells management that if everything else stays constant the actual profit will likely exceed the planned profit.

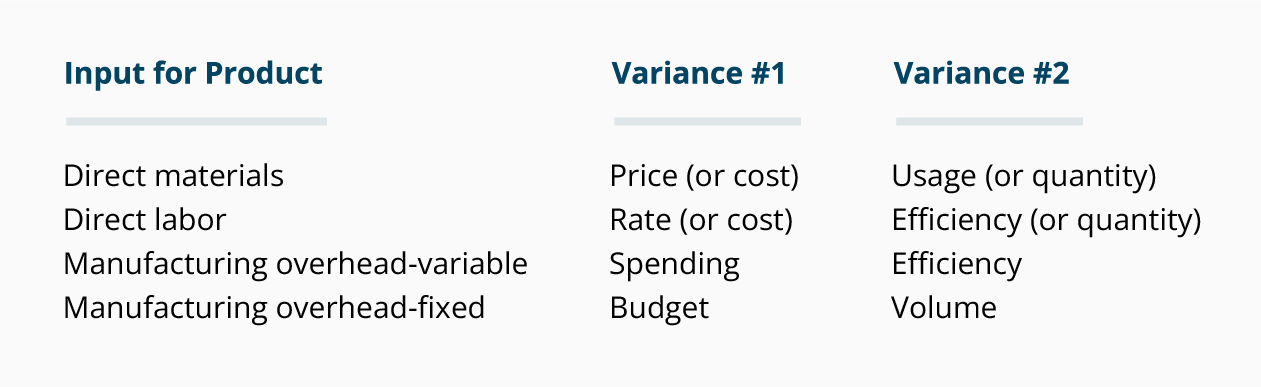

If we assume that a company uses the perpetual inventory system and that it carries all of its inventory accounts at standard cost (including Direct Materials Inventory or Stores), then the standard cost of a finished product is the sum of the standard costs of the inputs:

- Direct material

- Direct labor

- Manufacturing overhead

- Variable manufacturing overhead

- Fixed manufacturing overhead

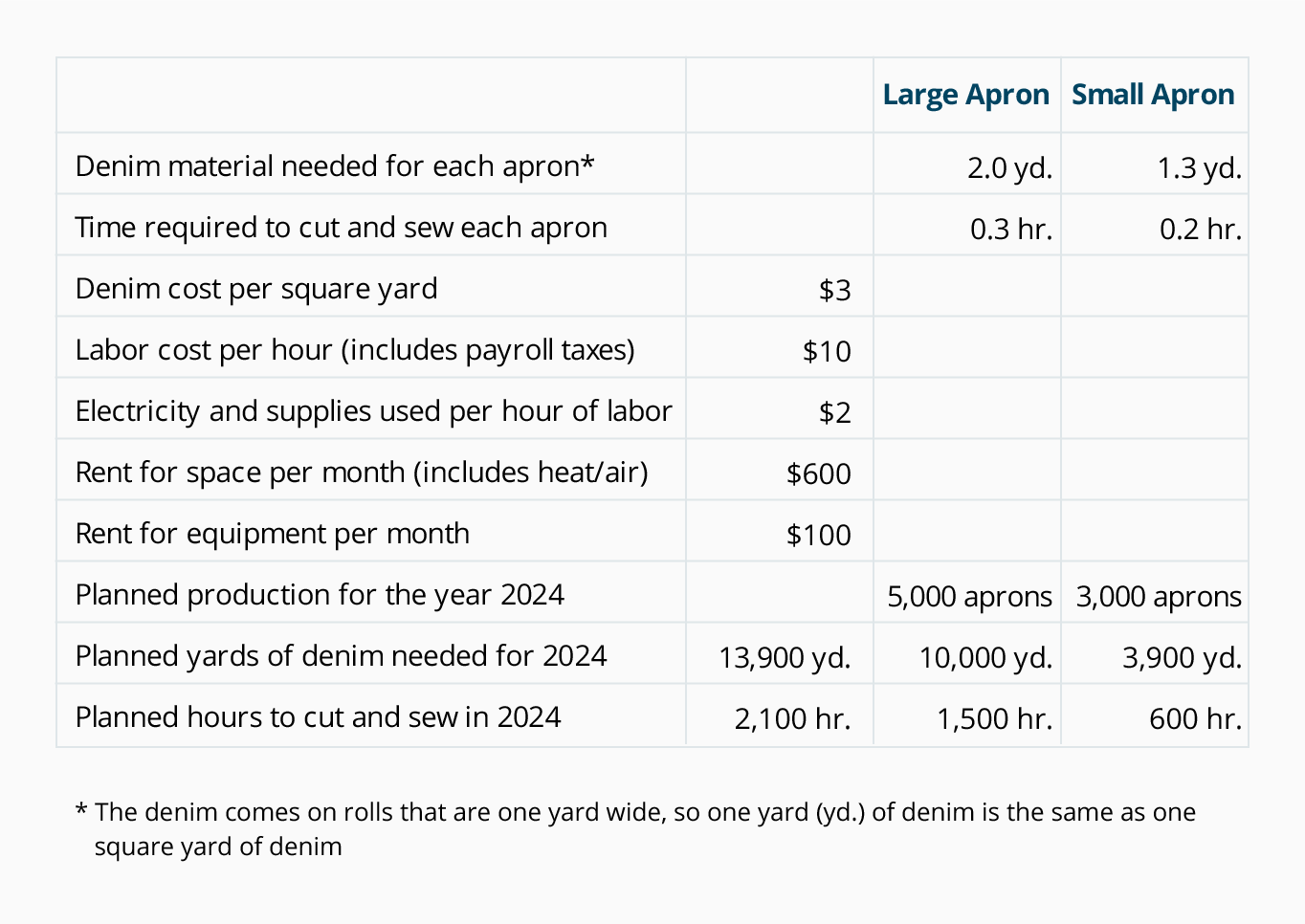

Sample Standards Table

Let's assume that your Uncle Pete runs a retail outlet that sells denim aprons in two sizes. Pete suggests that you get into the manufacturing side of the business, so on January 1, 2013 you start up an apron production company called DenimWorks. Using the best information at hand, the two of you compile the following estimates to use as standards for 2013:Standards Table for DenimWorks

The aprons are easy to produce, and no apron is ever left unfinished

at the end of any given day. This means that your company never has work-in-process inventory.

The aprons are easy to produce, and no apron is ever left unfinished

at the end of any given day. This means that your company never has work-in-process inventory. When we make your journal entries for completed aprons (shown below), we'll use an account called Inventory-FG which means Finished Goods Inventory. (Some companies will use WIP Inventory or Work-in-Process Inventory). We'll also use the account Direct Materials Inventory. (Other account titles often used for direct materials are Raw Materials Inventory or Stores.)

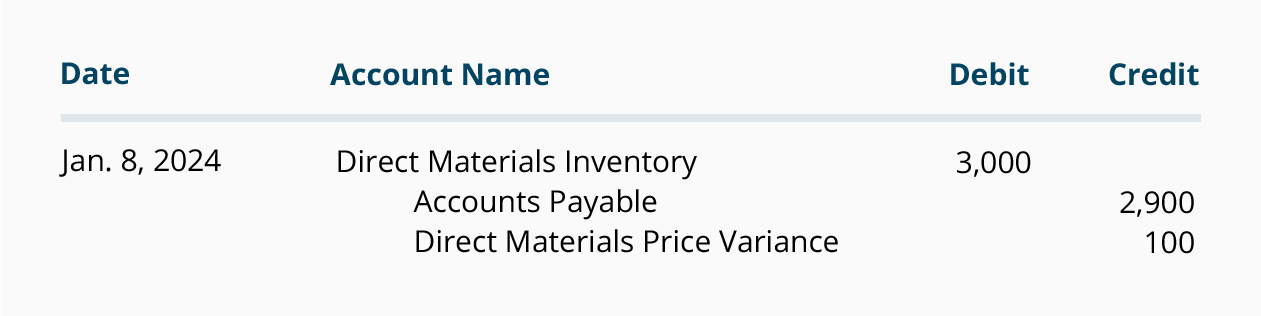

Direct Materials Purchased: Standard Cost and Price Variance

Direct materials refers to just that—raw materials that are directly traceable into a product. In your apron business the direct material is the denim. (In a food manufacturer's business the direct materials are the ingredients such as flour and sugar; in an automobile assembly plant, the direct materials are the cars' component parts).DenimWorks purchases its denim from a local supplier with terms of net 30 days, FOB destination. This means that title to the denim passes from the supplier to DenimWorks when DenimWorks receives the material. When the denim arrives, DenimWorks will record the denim received in its Direct Materials Inventory at the standard cost of $3 per yard (see standards table above) and will record the liability at the actual cost for the amount received. Any difference between the standard cost of the material and the actual cost of the material received is recorded as a purchase price variance.

Examples of Standard Cost of Materials and Price Variance

Let's assume that on January 2, 2013 DenimWorks ordered 1,000 yards of denim at $2.90 per yard. On January 8, 2013 DenimWorks receives 1,000 yards of denim and an invoice for the actual cost of $2,900. On January 8, 2013 DenimWorks becomes the owner of the material and has a liability to its supplier. On January 8 DenimWorks' Direct Materials Inventory is increased by the standard cost of $3,000 (1,000 yards of denim at the standard cost of $3 per yard), Accounts Payable is credited for $2,900 (the actual amount owed to the supplier), and the difference of $100 is credited to Direct Materials Price Variance. In general journal format the entry looks like this: The $100 credit to the price variance account communicates

immediately (when the denim arrives) that the company is experiencing

actual costs that are more favorable than the planned, standard cost.

The $100 credit to the price variance account communicates

immediately (when the denim arrives) that the company is experiencing

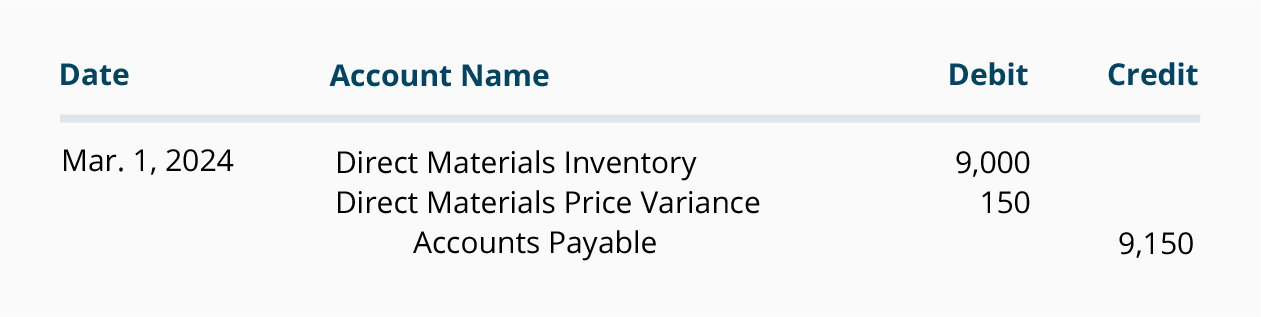

actual costs that are more favorable than the planned, standard cost.In February, DenimWorks orders 3,000 yards of denim at $3.05 per yard. On March 1, 2013 DenimWorks receives the 3,000 yards of denim and an invoice for $9,150 due in 30 days. On March 1, the Direct Materials Inventory account is increased by the standard cost of $9,000 (3,000 yards at the standard cost of $3 per yard), Accounts Payable is credited for $9,150 (the actual cost of the denim), and the difference of $150 is debited to Direct Materials Price Variance as an unfavorable price variance:

After the March 1 transaction is posted, the Direct Materials Price

Variance account shows a debit balance of $50 (the $100 credit on

January 2 combined with the $150 debit on March 1). A debit balance in a

variance account is always unfavorable—it shows that the total of

actual costs is higher than the total of the expected standard costs. In

other words, your company's profit will be $50 less than planned unless

you take some action.

After the March 1 transaction is posted, the Direct Materials Price

Variance account shows a debit balance of $50 (the $100 credit on

January 2 combined with the $150 debit on March 1). A debit balance in a

variance account is always unfavorable—it shows that the total of

actual costs is higher than the total of the expected standard costs. In

other words, your company's profit will be $50 less than planned unless

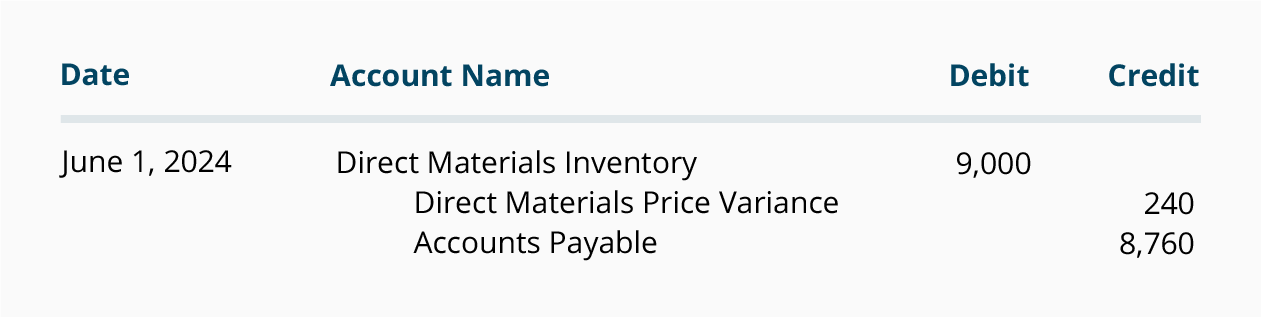

you take some action.On June 1 your company receives 3,000 yards of denim at an actual cost of $2.92 per yard for a total of $8,760 due in 30 days. The entry is:

Direct Materials Inventory is debited for the standard cost of $9,000

(3,000 yards at $3 per yard), Accounts Payable is credited for the

actual amount owed, and the difference of $240 is credited to Direct

Materials Price Variance. A credit to the variance account indicates

that the actual cost is less than the standard cost.

Direct Materials Inventory is debited for the standard cost of $9,000

(3,000 yards at $3 per yard), Accounts Payable is credited for the

actual amount owed, and the difference of $240 is credited to Direct

Materials Price Variance. A credit to the variance account indicates

that the actual cost is less than the standard cost.After this transaction is recorded, the Direct Materials Price Variance account shows an overall credit balance of $190. A credit balance in a variance account is always favorable. In other words, your company's profit will be $190 greater than planned due to the favorable cost of direct materials.

Note that the entire price variance pertaining to all of the direct materials received was recorded immediately. In other words, the price variance associated with the direct materials received was not delayed until the materials were used.

No comments:

Post a Comment